Asset Finance

Redesigning SME Lending & Asset Finance for the Digital Era

Client: Lloyds Banking Group, Commercial Bank, London

Sector: Financial Services – Business Banking

Role: Senior Manager & Service Design Lead

Role: Senior Manager & Service Design Lead

BUSINESS CHALLENGE

The COVID-19 pandemic reshaped how small and medium-sized businesses accessed financial products.

• 78% of SMEs reported being more reliant on digital banking than ever before.

• 89% expected more digital services post-pandemic.

Yet, banks still relied heavily on relationship manager (RM)-led processes. While valued for trust, these were slow, complex, and ill-suited to the urgency and convenience SME owners demanded.

The business lending process needs to change to compete with digital-first lenders while preserving the human touch that builds trust at critical decision points.

CUSTOMER PROBLEM

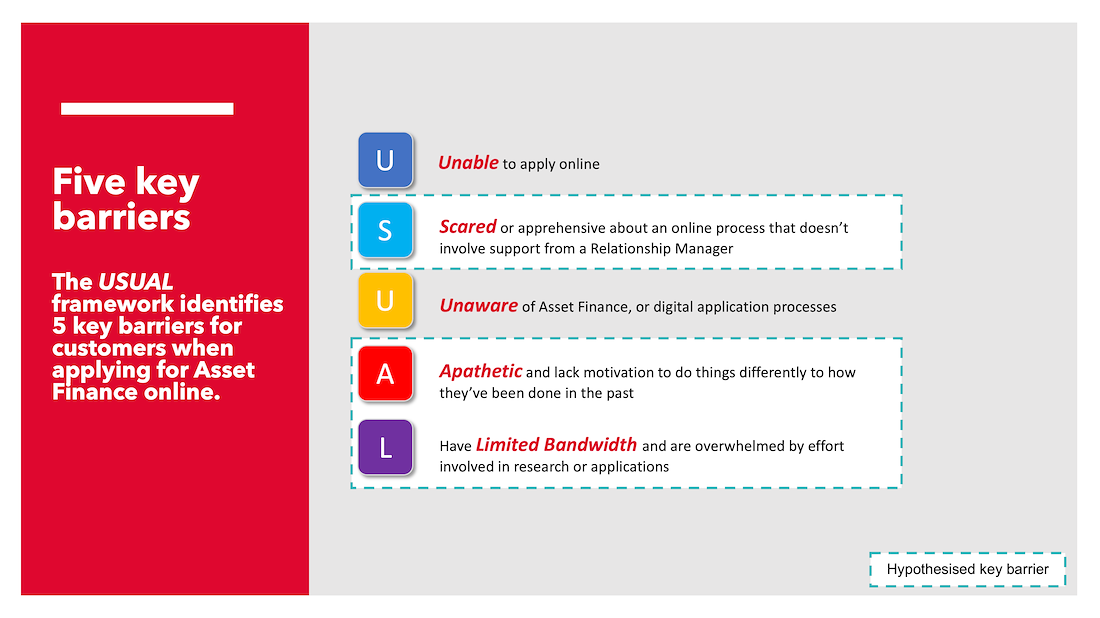

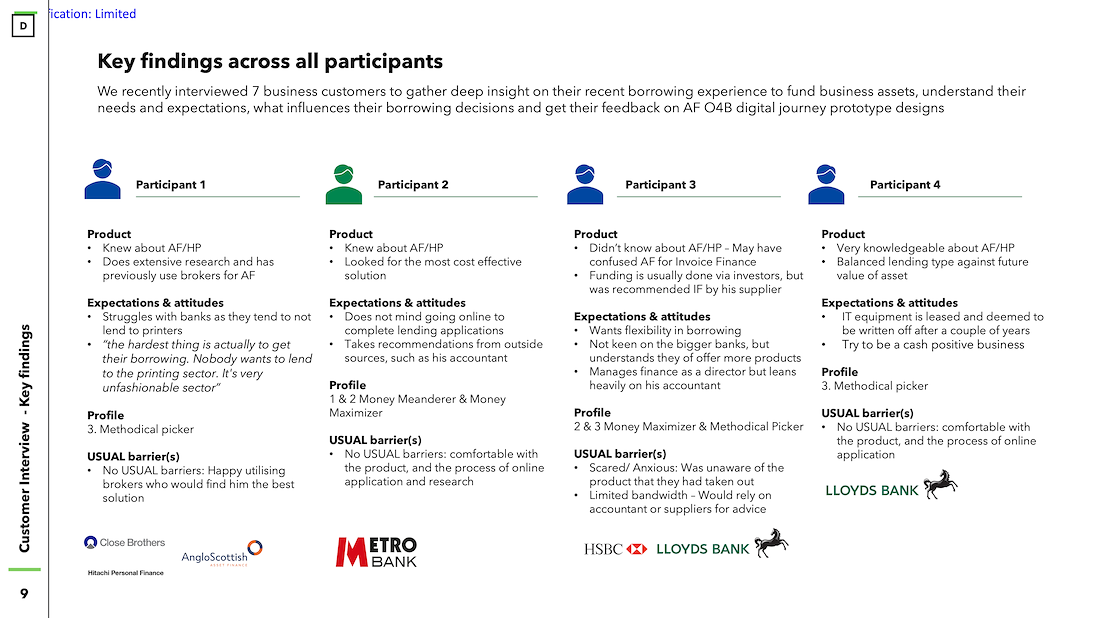

Through surveys, behavioural science (USUAL framework), and in-depth interviews, we identified recurring pain points across Lending and Asset Finance:

Complexity & Overwhelm: 81% of SMEs said research felt complex; 67% struggled with limited time/bandwidth.

Fear of Mistakes: Many SMEs feared making the wrong choice without RM reassurance.

Trust & Transparency: Customers valued speed, but wanted clarity on eligibility, pricing, and next steps before committing.

Moments for Human Touch: Decision points above £100k or for applications that require partner approval need reassurance from a person.

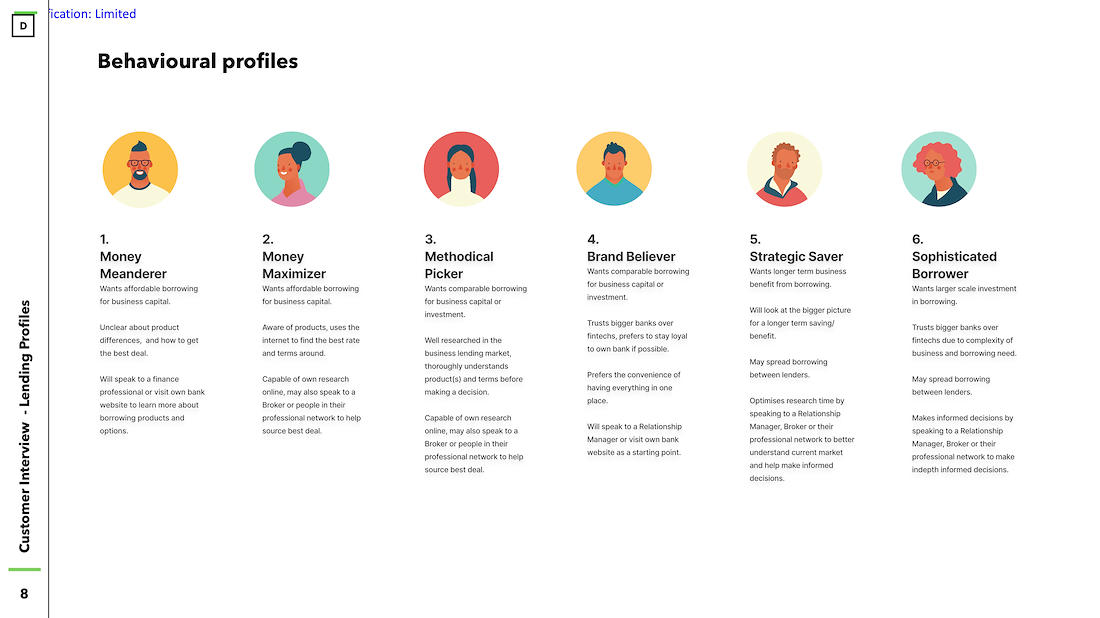

RESEARCH & DESIGN APPROACH

We ran a multi-stage human-centred design phase:

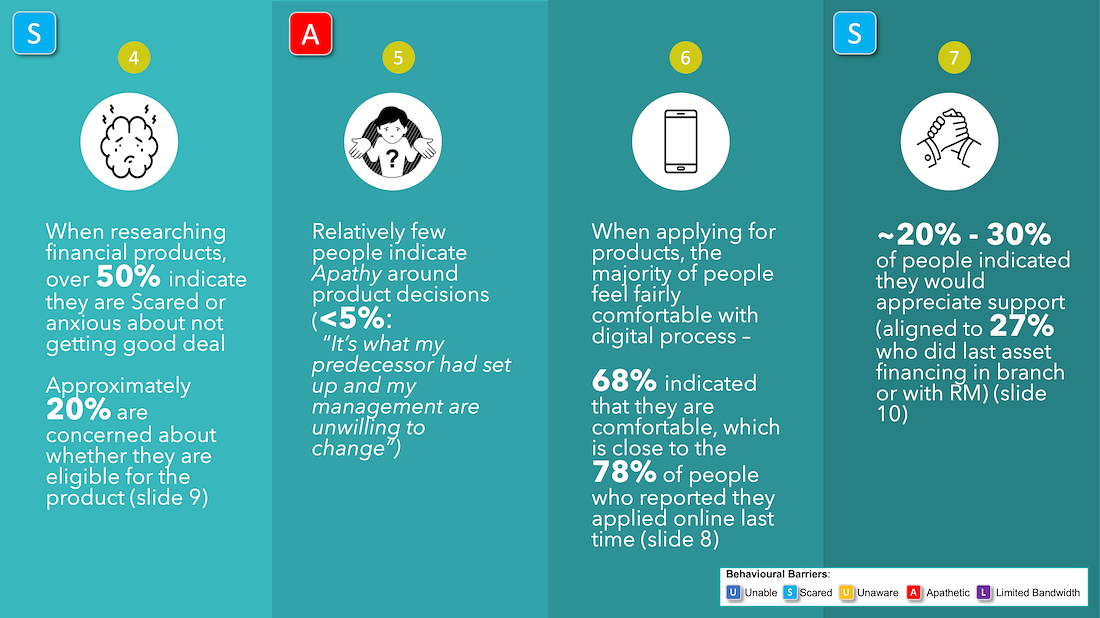

• Quantitative survey (149 SMEs) to identify behavioural barriers to digital adoption.

• Customer interviews & journey mapping to uncover pain points in “as-is” processes.

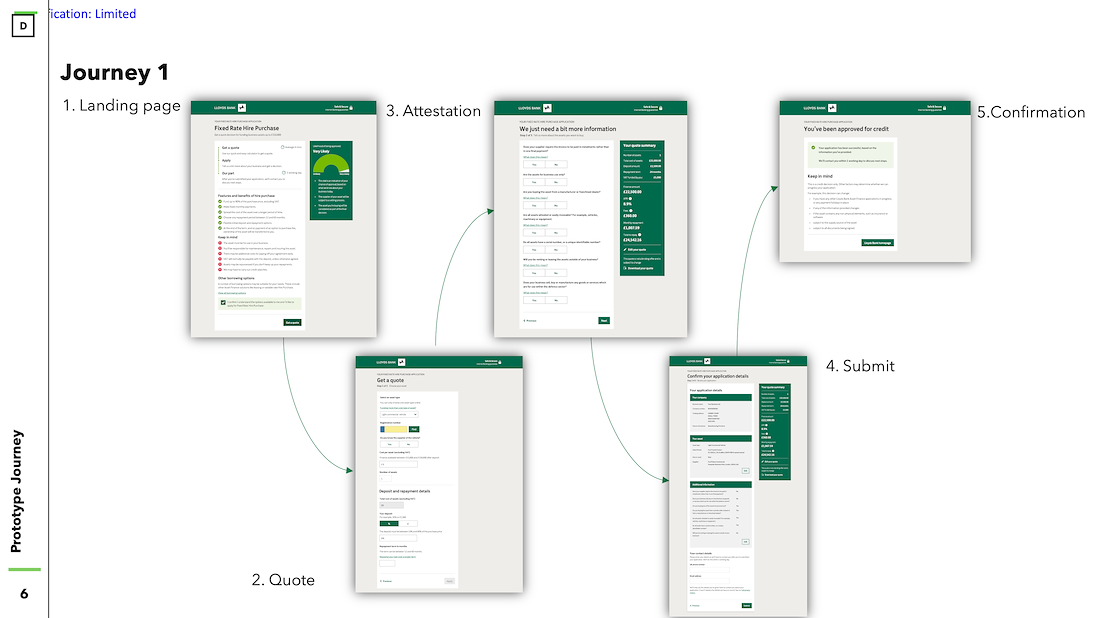

• Prototype testing (2 rounds, 7 participants each) to validate and refine digital journeys.

• Behavioural science (USUAL framework) to identify five adoption blockers: Unable, Unaware, Scared, Limited Bandwidth, Apathetic.

This multi-lens approach, combining behavioral design, UX, and service design, gave us clarity on why SMEs weren’t adopting digital journeys and what design interventions could unlock engagement.

We designed and tested prototypes to tackle four core areas of improvement:

Supplier Accreditation: manual, opaque, heavily RM-dependent: Create a digital accreditation flow that builds trust without endless back-and-forth.

Complex Application Journeys: phone calls, PDFs, manual signatures: Streamline into a self-serve flow while surfacing support only when needed.

Customer Confidence & Transparency: lack of visibility into progress, timelines, and what comes next: Introduce progress trackers, clear confirmation screens, and eligibility calculators.

Balancing Digital with Human Touch: RMs were central to every step, slowing down deals: Reframe RMs as escalation points at key “moments of truth,” not gatekeepers.

TARGETED IMPROVEMENTS

• Self-Serve Quote Tool: Instant, realistic quotes aligned to internal pricing models, reducing research anxiety.

• Progress Tracker: Persistent navigation bar to set expectations and reduce abandonment.

• Supplier Accreditation Portal: API-driven, risk-based accreditation with options for supplier self-certification.

• Save & Resume: Enabled SMEs to pause, consult with partners/accountants, and return without restarting.

• Hybrid Human Touch: Embedded RM escalation for high-value or complex cases, ensuring digital trust without losing personal support.

• Copy & Content Design: Plain-language rewrites (tested iteratively) that reduced confusion and helped SMEs feel in control.

BUSINESS IMPACT

• Faster Response and Delivery: Prototype journey reduced decision steps, with quotes and eligibility available in minutes rather than days.

• Operational Efficiency: Supplier accreditation automation reduced back-office rework and fraud risk.

• Customer Empowerment: SMEs reported journeys felt “straightforward” and “playable” — echoing consumer-grade expectations.

• Market Differentiation: Positioned the bank against fintechs by combining digital ease with human trust.

REFLECTION

This project was executed under the dual pressure of:

• COVID-19 digital acceleration: Forcing customers to transact online.

• Competitive disruption: Fintechs offering speed but not necessarily trust.

As I led the design team, we operated as an incubation lab, balancing user needs, business risk, and technical feasibility. By weaving customer research, behavioural science, and iterative prototyping, we reframed SME lending into a hybrid digital experience, one that meets modern expectations without losing the human reassurance businesses still value.